-

-

0 Comments

I’ll regularly think about organising my first checking account as a toddler. My mom drove me over to the native monetary establishment to rearrange a monetary financial monetary financial savings account the place I would deposit cash and checks, along with annual birthday presents from family and one different money I purchased proper right here all via at a youthful age.

As rapidly as I used to be 16, my mom took me to the grocery retailer division of a Nationwide monetary establishment to get my first checking account. Whereas this “free checking for all occasions,” didn’t pretty dwell as heaps as its title, having a checking account did give me entry to a financial system that many People don’t have the information or potential to learn from.

Looking at households that seem similar to the one I grew up in, I figured all of us took checks to the monetary establishment to make a deposit. I assumed most people would ship money to others using a look at, or later an web service like Venmo or PayPal. As an grownup, I seen that is removed from the case.

What’s Ahead:

- Who’s unbanked and underbanked?

- Why are some households unbanked and underbanked?

- Accessing your payroll from work

- Paying the gasoline or vitality bill

- Making a purchase order order order order the place solely debit or financial institution having fun with taking part in playing cards are accepted

- Sending money to family or buddies

- Borrowing money

- Saving money for emergencies and long-term targets

- Listed beneath are some options for the unbanked and underbanked

- Summary

Who’s unbanked and underbanked?

Being unbanked means an individual or family has no typical monetary establishment accounts within the least. Underbanked households have a checking or monetary financial monetary financial savings account nonetheless along with use fairly just a few financial suppliers resembling money orders, look at cashing, worldwide remittances, payday loans, refund anticipation loans, rent-to-own suppliers, pawnshop loans, or auto title loans, based mostly completely on the FDIC.

Whereas about 97% of white households have all of their banking wants met, the numbers is not going to be almost the equal for America’s minority populations. 2017 data from the FDIC exhibits that 3% of white households are unbanked. However, about 17% of black and 14% of Hispanic households don’t have monetary establishment accounts. Whilst you broaden that to include the underbanked, people who have accounts nonetheless lack entry to some wanted banking suppliers, about 30% of black households and 29% of Hispanic households are missing out.

Consistent with the 2017 FDIC Nationwide Survey of Unbanked and Underbanked Households, the almost positively populations to not be totally banked are lower-income households, less-educated households, youthful households, black and Hispanic households, working-age disabled households, and households with unstable earnings.

Why are some households unbanked and underbanked?

Consistent with the FDIC survey, there are a group of frequent causes U.S. households don’t have a checking account.

- Not adequate money: Larger than half of these which could possibly be unbanked say that they don’t afford to look after in an account. That’s the commonest motive to not have a checking account.

- Don’t notion banks: About 30% of respondents acknowledged that they “don’t notion banks.” That’s the second commonest motive to not have a checking account.

- Monetary establishment prices: The third commonest motive to not have a checking account is monetary establishment prices. Many people acknowledged that prices have been each too extreme or too unpredictable.

Whereas these are frequent causes to not have a checking account, the best reply is deciding on a monetary establishment chances are you’ll notion that offers low-fee accounts with no minimal steadiness requirements. Whereas you choose an account with no recurring prices and favorable worth buildings for patrons, chances are you’ll rest easy that your money is protected, insured, and gained’t be matter to shock funds.

Some buyers don’t have accounts because of they don’t seem to be conveniently within the market or they lack financial literacy. If there will not be any shut by banks, it is not going to be attainable for loads of People to open a checking account even after they do have the money and time to take motion. Presumably the best selections for this, if internet entry is accessible, is to rearrange an web account by way of Chime.

Accessing your payroll from work

Consistent with NACHA, the group accountable for managing the nation’s direct deposit system, 82% of People are paid through direct deposit. Nonetheless for those who occur to don’t have a checking account, getting paid through direct deposit isn’t an alternate.

You moreover don’t have the facility to deposit your paycheck into your checking account collectively alongside collectively together with your cellphone, a free service that takes decrease than 30 seconds. As an alternative, it is very important cash your paycheck with a check-cashing service. It’d appear to be this:

- Cash the look at on the issuing monetary establishment: Most banks will cash a look at drawn on a purchaser’s account. Some value a flat worth of some {{{{dollars}}}} for this service whereas others will do it totally free. Each methodology, it is very important make a journey to the look at creator’s monetary establishment, not your particular particular person, to do this.

- Cash the look at at a grocery retailer: Grocery retailer chains like Walmart and Kroger present look at cashing partially because of they hope you may spend your money there. Walmart funds $4 or $8 to cash a look at. At Kroger-owned retailers, prices start at $3 per look at cashed and differ by state.

- Payday mortgage or look at cashing retailers: Payments are often elevated at check-cashing or payday mortgage amenities. They often require a flat-fee plus a proportion of the look at amount.

I had positively not tried to cash a payroll look at until numerous years beforehand after I participated in FinX from the Coronary coronary coronary heart for Financial Suppliers Innovation. I was despatched into Hollywood with a payroll look at and a list of errands. Sooner than even attending to the errands, I had misplaced about 7% of my look at to prices whereas spending over a half hour getting the cash. Nonetheless that’s widespread with no checking account.

Paying the gasoline or vitality bill

When your electrical vitality, gasoline, or water bill exhibits up in your mailbox or piece of email correspondence inbox, you may want it set to pay mechanically with a checking account, financial institution card, or debit card. Nonetheless for those who occur to don’t have these accounts, it’s important to pay one completely totally different methodology.

As an alternative of paying totally free with numerous taps in your cellphone or clicks in your laptop computer laptop current, paying utilities with no checking account requires a bit additional effort. You possibly can be succesful to pay at an space office or grocery retailer, nonetheless chances are you’ll’t steadily pay with cash and in addition to you may ought to pay additional processing prices for those who occur to go this route.

Utterly completely totally different options embrace mailing a money order, which takes a worth of some {{{{dollars}}}}, a stamp, and an envelope or a pay as you go debit card, which moreover requires prices and extra time to load the cardboard.

In any case, paying funds with no checking account takes far more time and generally extra cash. In some methods, it’s like an added tax for being poor or not understanding about how the banking system works.

Making a purchase order order order order the place solely debit or financial institution having fun with taking part in playing cards are accepted

Debit having enjoyable with having fun with taking part in playing cards, and generally financial institution having fun with taking part in playing cards, are one completely totally different financial service most people take as a right. You presumably can merely take that card anyplace you go and swipe it to pay. Usually, you gained’t pay any further prices.

Nonetheless what about companies that don’t take any cash? If you happen to want to retailer on-line at Amazon, journey in an Uber, or go to a enterprise that doesn’t take cash, you need a plastic card to pay. With out it, you presumably can ought to pay additional to purchase at an space retailer as a substitute of on-line or pay additional for the standard cab as a substitute of a ride-hailing service.

The reply appropriate correct proper right here is one completely totally different one which comes with further prices and presumably sucks up hours of time. Pay as you go having enjoyable with having fun with taking part in playing cards, which you often see at consolation retailers and grocery retailers, offer you a number of the options of a debit card. However, you generally ought to pay to buy one, pay to load them, and have further prices counting on the way in which you benefit from the account.

As rapidly as I attempted one out by way of the FinX experience, I spent about $5 in prices to buy and cargo a card and it didn’t even work. After a half-hour on the cellphone prepared and chatting with purchaser assist, my crew realized the money could be locked up for a day or additional.

Whilst you’re already residing paycheck-to-paycheck, which will lead to late prices or skipping dinner in your family members members. Pay as you go having enjoyable with having fun with taking part in playing cards are okay as rapidly as they work, nonetheless they’re nonetheless a further expense low-income of us ought to pay that these with monetary establishment accounts don’t.

Sending money to family or buddies

When splitting a value with family or buddies, or sending money for a further motive, of us with monetary establishment accounts can use free suppliers like Venmo, Sq. Cash, or Zelle to ship funds shortly to anyone else with an account.

Everytime you don’t have a checking account, nonetheless, these accounts gained’t work as supposed. You might nonetheless be succesful to entry some selections, nonetheless you clearly can’t swap to or from a linked checking account.

As an alternative, most unbanked and underbanked buyers look to paid suppliers to ship funds. Which is able to embrace mailing a money order or cashier’s look at or using a swap service like Western Union or MoneyGram.

Western Union funds based totally fully on the place you are sending funds. To hunt out out exactly what it will worth, I checked on the worth for swap contained inside the U.S. the place you pay cash in a retailer. For a $500 swap, you’d pay $15, or 3%. Plus, it takes time to go to the store to drop off the money and put collectively the swap. That gives as heaps as an infinite worth you don’t ought to pay everytime you’ve purchased an steadily checking account.

Borrowing money

Many people with monetary establishment accounts moreover produce completely totally different typical financial merchandise like financial institution having fun with taking part in playing cards, auto loans, and residential loans. Nonetheless qualifying for the standard mortgage is not going to be attainable with no checking account.

These with a satisfactory credit score rating ranking rating can use a financial institution card in a pinch, which ceaselessly carries an cost of curiosity of spherical 10% to 29% relying in your credit score rating ranking rating historic earlier. Non-public loans and secured loans might present lower prices in some circumstances.

Whilst you’ve purchased poor credit score rating ranking rating and don’t have entry to simple banking, frequent sources of funds all through troublesome financial intervals embrace payday loans, auto title loans, and pawnshop loans.

Payday loans are notably worrisome, as they often carry triple-digit costs of curiosity. Whereas 16 states and Washington D.C. now cap costs of curiosity at 36% or heaps lots a lot much less, the frequent annual proportion value (APR) for these loans is 391%, based mostly completely on the Coronary coronary coronary heart for Accountable Lending. Which means debtors would pay the principal as quickly as additional numerous circumstances over yearly contained in the occasion that they recurrently lengthen the mortgage.

Saving money for emergencies and long-term targets

Everytime you don’t afford to look after a checking account, you presumably don’t have adequate for long-term monetary financial monetary financial savings. However when chances are you’ll scrape the funds collectively to put one challenge away for a moist day, the place do you keep it for those who occur to don’t have a checking account?

Whereas banks present security and FDIC insurance coverage protection safety security, cash-based households might protect extra money spherical the house, in a automotive, beneath a mattress, or buried in a can contained within the yard. Really!

There are a complete lot of things with stashing cash spherical your property. The money is also misplaced or stolen. It could possibly be destroyed in a fire, flood, or totally completely totally different accident. And it doesn’t earn any curiosity.

Considerably than put it apart, nonetheless, many low-income households are compelled to spend their money on elementary wants like groceries and lease.

Listed beneath are some options for the unbanked and underbanked

Everytime you don’t have a checking account or the useful mobile banking app that comes along with it, financial suppliers look very totally totally completely totally different. Essential duties like cashing a paycheck or paying in your dwelling utilities are loads additional sturdy, and generally costlier.

Many lower-income households look to payday lenders, look at cashing companies, pawnshops, automotive title lenders, and totally completely totally different usually predatory suppliers to fulfill their money wants. As an alternative, will almost certainly be greater to open a typical checking account at a monetary establishment that helps prospects succeed with their money.

And under no circumstances utilizing a checking account, elementary financial suppliers like money orders and look at cashing may merely add as heaps as $500 in annual funds the place these with a checking account can do that stuff totally free.

Listed beneath are examples of no-fee and low-fee banks which could possibly be good for folks opening a checking account for the first time or are returning to banking after a interval away:

Chime

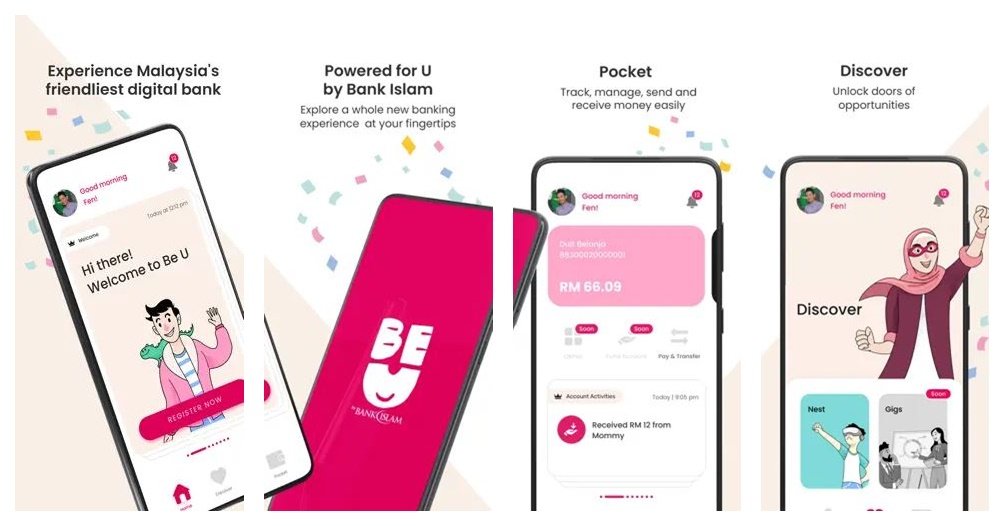

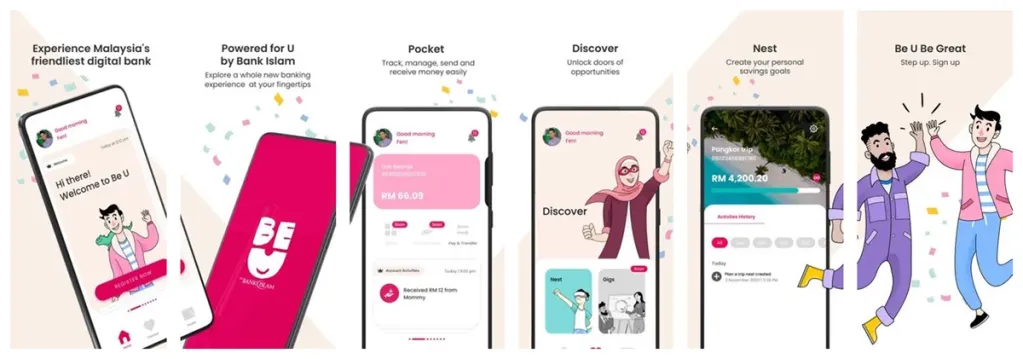

Chime is an online-only app that offers an outstanding checking account with no minimal steadiness and no recurring prices. Chime comprises a wide range of additional selections at no added worth. Depositing a look at collectively alongside collectively together with your cellphone, paying funds, and totally completely totally different elementary financial duties are merely handled contained within the mobile app.

There will not be any month-to-month prices, worldwide transaction prices, minimal steadiness prices, service prices, debit card completely totally different prices, or prices for on-line transfers to totally completely totally different banks. You presumably can actually use this account totally free with out finish in fairly just a few circumstances. That makes it an unimaginable various for anyone with a smartphone that ought to care for his or her money with a protected and dependable account at work, dwelling, or on the go.

Chime Disclosure – *Chime is a financial know-how firm, not a monetary establishment. Banking suppliers and debit card provided by The Bancorp Monetary establishment or Stride Monetary establishment, N.A.; Members FDIC.

(1)Save As rapidly as I Get Paid mechanically transfers 10% of your direct deposits of $500 or additional out of your Checking Account into your monetary financial monetary financial savings account.

^Spherical Ups mechanically spherical up debit card purchases to the closest buck and swap the spherical up out of your Chime Checking Account to your monetary financial monetary financial savings account.

Novo

Novo is an environment friendly fintech firm for small companies looking for to stay away from frequent enterprise banking prices. Optimized for neutral enterprise homeowners, entrepreneurs, and freelancers, Novo accounts have no hidden prices and make managing your enterprise funds easy.

The account makes most enterprise wants free along with ACH transfers, mailed bill value checks, mobile look at deposits, incoming wires, and ATM visits. Novo even mechanically refunds totally completely totally different monetary establishment’s ATM prices. Everytime you’re in quest of a small enterprise monetary establishment with only some prices and no minimal steadiness requirements, Novo is an atmosphere pleasant various.

Summary

Whilst you’ve purchased an account with a high-quality monetary establishment, you gained’t ought to pay any recurring prices and don’t have to stress about minimal balances. You presumably can deposit checks using your cellphone and ship funds to household and buddies totally free in only some moments.

Every American might want to have entry to a high quality checking account with low prices, nonetheless that merely isn’t the case in the interim. By serving to additional of us get entry to the U.S. banking system, all of us benefits.

Study additional:

- Banking 101—A Info For Youngsters (And Anyone Who Needs A Refresher)

- Most fascinating Extreme Yield Monetary financial monetary financial savings Accounts In distinction

,

(Image credit score rating score rating: Mandel Ngan/Getty Footage)

(Image credit score rating score rating: Mandel Ngan/Getty Footage)

(Image credit score rating score rating: Shutterstock) Rachel Stephens

(Image credit score rating score rating: Shutterstock) Rachel Stephens

(Image: The Edge Markets)

(Image: The Edge Markets)

(Image: Microsoft)

(Image: Microsoft) (Image: AsiaOne)

(Image: AsiaOne)

(Image: Malay Mail/Shafwan Zaidon)

(Image: Malay Mail/Shafwan Zaidon)

(Image: The Malaysian Reserve)

(Image: The Malaysian Reserve) (Image: Malay Mail/Shafwan Zaidon)

(Image: Malay Mail/Shafwan Zaidon)

(Image: HRNEWS.my)

(Image: HRNEWS.my)

(Image credit score rating score rating: Pixabay)

(Image credit score rating score rating: Pixabay)

(Image: The Malaysian Reserve)

(Image: The Malaysian Reserve)

(Image credit score rating score rating: Pixabay)

(Image credit score rating score rating: Pixabay)